{kind=link}

Cash is the lifeblood of every business—especially new and small businesses.

While there are many hurdles for small businesses, limited or inconsistent cash flow is one of the tallest. A study by US Bank shows that82% of small businessesfail because of cash flow issues.

In other words,with no cash, there is no business. That’s why understanding andmanaging cash flowis a prerequisite for success.

To get a grasp of the money coming into and going out of your business, you need a cash flow statement. If you’re having a hard time with financial statements, don’t worry—we’ll help you put your cash flow statement together.

什么是现金流量表?

A cash flow statement (CFS) is a financial statement that summarizes the inflows and outflows of cash transactions during a given period.

The purpose of a cash flow statement is to record the amount of cash and cash equivalents entering and leaving the company. As a result, businesses get a detailed picture of the cash position, which is essential for the company'’ financial health. You can prepare a cash flow statement in a spreadsheet or find it in yoursmall business accounting software.

Many small businesses fall into the trap of focusing too much on profit/loss and ignoring cash flow. So they end up running out of cash without knowing how it happened. Having a clear overview of your cash flow will allow you to understand where the money is coming from and how it is spent. Ultimately, this will help you make more informed business decisions.

The key elements of a cash flow statement

A cash flow statement typically includes three main components:

- Operating activities

- Investing activities

- Financing activities

Cash flow from operating activities

The operating activities of the cash flow statement include activities related to the core business. In other words, this section measures the cash flow from a company’s provision of products or services. Some examples of operating activities include sales of goods and services, salary payments, rent payments, and income tax payments.

Cash flow from investing activities

Investing activities include cash flow from the acquisition and disposal of long-term assets and other investments not included in cash equivalents. These represent long-term investments in the company’s growth. For instance, purchasing or selling physical property, such as real estate or vehicles, and non-physical property, like patents.

Cash flow from financing activities

Cash flows related to financing activities typically represent cash from investors or banks, issuing and buying back shares, as well as a dividend payment. So whether you areraising a loan, paying interest to service debt, or distributing dividends, all these transactions fall under the financing activities section in the cash flow statement.

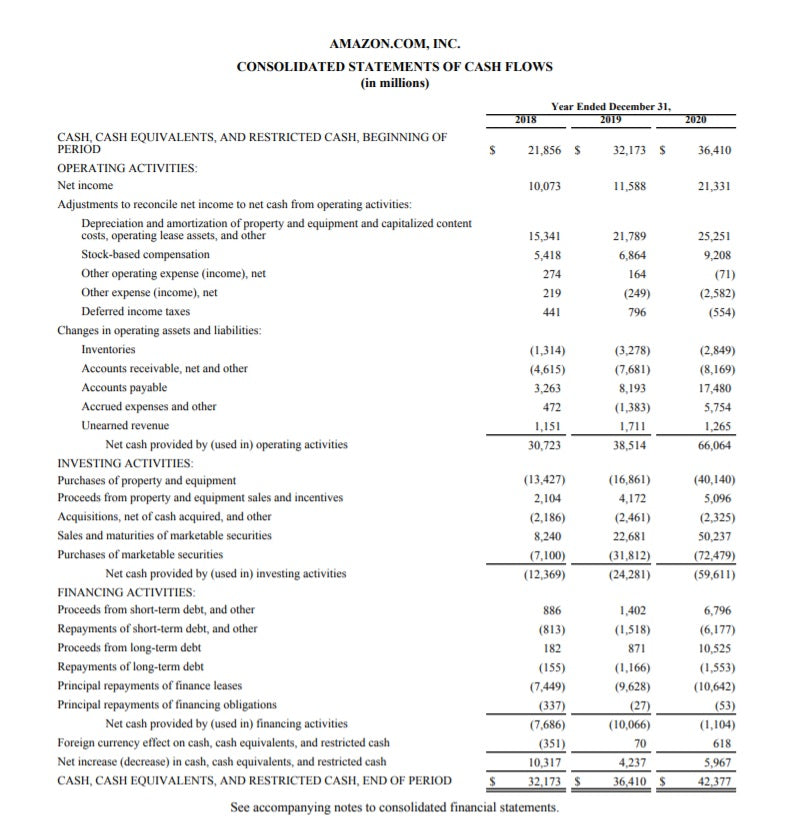

Here’s an example of Amazon’s cash flow statement from its2020 annual report. You can see the three main sections: operating activities, investing activities, and financing activities.

The cash flow statement starts with cash on hand and net income. After calculating cash inflows and outflows from operating activities, Amazon posted $66.06 billion in cash from operating.

Investing activities were -$59.61 billion, primarily due to purchases of property and equipment, as well as marketable securities. Financing activities were -$1.1 billion.

At the end of 2020, Amazon had $42.37 billion in cash on hand.

Image source:Amazon

Difference between a cash flow and other financial statements

Financial statementsare reports that summarize the financial performance of your business. The cash flow statement is one of the three main types of financial statements, alongside thebalance sheetandincome statement.

In a nutshell, an income statement measures revenue, expenses, and profitability. On the other hand, a balance sheet shows the assets, liabilities, and shareholders’ equity. And finally, a cash flow statement records the increases and decreases in cash.

All three financial statements are different, but they are intricately linked. Net income from the income statement feeds into retained earnings on the balance sheet, and it is the starting point in the cash flow statement.

Here’s a comparison of the three financial statements:

| Income statement | Balance sheet | Cash flow | |

| Time | Period of time | A point in time | Period of time |

| Purpose | Profitability | Financial position | Cash movements |

| Measures | Revenue, expenses, profitability | Assets, liabilities, shareholders' equity | Increases and decreases in cash |

| Starting point | Revenue | Cash balance | Net income |

| Ending point | Net income | Retained earnings | Cash balance |

Source:Corporate Finance Institute

Now that we’ve covered the basics of a cash flow statement, let’s look at the two calculating methods: the direct method and the indirect method.

Cash flow calculation methods

The direct method includes all the inflows and outflows of cash from operating activities.This method is based on thecash basis accounting modelthat recognizes revenues when cash is received and expenses when they are paid. The direct method is straightforward, but it requirestracking every cash transaction, so it might require more effort.

Analyzing a cash flow statement requires understanding the context so you can make informed decisions based on the numbers you see. What stage is the business in? Is it a growing startup or a mature enterprise? The most important thing to remember is that the cash flow statement doesn’t reflect the profitability of your business but rather the cash inflows and outflows.

Pros:

- Transparent

- Easy to understand

- Uses real-time figures

Cons:

- It takes more time and effort

- It can be an issue for businesses that use accrual accounting

- Businesses that use the direct method still need to disclose a reconciliation of net income to cash flow from operating activities

The indirect method calculates the cash flow by adjusting net income with differences from non-cash transactions.This method is especially suitable for businesses using theaccrual basis accounting, where revenue is recorded when it is earned rather than when it is received. When using the indirect method, you begin with the net income from the income statement and make adjustments to undo the impact of accruals made during the period.

Pros:

- Easy to prepare

- Allows for reconciliation between two other financial statements—the income statement and balance sheet

- Discloses non-cash transactions

Cons:

- Lack of transparency

No matter which method you choose, it will affect only the operating activities section. The two other sections—cash from investing and financing activities—remain the same.

In this example, you can see that the indirect method uses net income as a base and adds non-cash expenses like depreciation and amortization. On the other hand, the direct method takes all cash collections from operating activities and subtracts the cash disbursements from operating activities, such as payments to suppliers and wages.

Indirect method |

Direct method |

||

Net income |

$400 |

Collections from customers |

$1,000 |

Adjustments |

Deductions |

||

Depreciation |

$100 |

Payments to suppliers |

($200) |

Amortization |

$100 |

Wages |

($200) |

Net cash from operating activities |

$600 |

Net cash from operating activities |

$600 |

How to read a cash flow statement

The goal of the cash flow statement is to show the amount of generated and spent cash over a specific period of time, and it helps businesses analyze the liquidity and long-term solvency.

When you summarize all cash transactions, you can get a positive or a negative cash flow.

Positive cash flowmeans you have more money coming in than going out. This opens up great opportunities for reinvesting the excess of cash in business growth. However, a positive cash flow doesn’t necessarily mean that your business is profitable. There are cases where the company has a negative net income, but it has a positive cash flow due to cash from borrowing.

Negative cash flow表明你花了更多的钱比你情况ated during a specific period of time. Is this a bad sign? The short answer: It depends. A negative cash flow isn’t necessarily a bad thing—especially if it results from investment in future growth. However, if you have a negative cash flow in more than one period, you should consider it a red flag. It can indicate that your business's financial health may be at risk.

This is particularly true for VC-funded startups, where the negative cash flow is also known as burn rate. This is the rate at which a new company is spending its venture capital to finance expensesbeforegenerating positive cash flow from its operations. The burn rate helps show how long you can continue your activity with the current overhead and revenue stream. A high burn rate is not uncommon for fast-growing startups, as it can help them gain market share, win customers, and generate higher long-term profits.

Cash flow statement example (+ template)

Now it’s your turn. Here’s afree cash flow templatethat you can customize to fit your needs.

第一步是开始填写现金落下帷幕OB欧宝娱乐APPance. Then continue by adding the cash from operations and additional cash received from activities such as sales of current assets, new investment received, etc.

The next step is subtracting the expenditures from operations and additional cash spent, like repayment of current borrowing, long-term liabilities repayment, etc.

After calculating the net cash flow, add the starting cash balance, and you’ll get the ending cash balance for the period.

Image source:Shopify

Image source:Shopify

You can also useShopify's cash flow calculatorto easily calculate your cash flow and give your business a financial health check in less than five minutes.

Cash Flow Statement FAQ

What is a cash flow statement statement?

What are the 3 types of cash flow statement?

- Operating Cash Flow – This reflects the cash inflows and outflows from the day-to-day operations of the business.

- Investing Cash Flow – This reflects the cash inflows and outflows from investments made by the company.

- Financing Cash Flow – This reflects the cash inflows and outflows from financing activities, such as taking out loans, issuing bonds or stock, or repaying debt.

What is cash flow example?

How do you calculate cash flow statement?

- Start with the net income: The first step in calculating cash flow is to determine the net income. This can be done by subtracting all expenses from sales or revenue.

- Add non-cash expenses: Non-cash expenses are those that are not paid with cash. These include depreciation, amortization and any losses from the sale of assets.

- Subtract any changes in working capital: Working capital is the difference between current assets and current liabilities. This can fluctuate from one period to the next and needs to be taken into account when calculating cash flow.

- Add other cash items: Other cash items include dividends paid, interest paid and any other cash investments or payments.

- Calculate the cash flow: The final step is to add the net income, non-cash expenses, any changes in working capital and other cash items. This should give you the total cash flow for the period.