{kind=link}

When a customer wants to buy an item but they don’t have the cash handy, they have a few options: put it on a credit card, use the store’s layaway program (if it has one), or opt for a buy now, pay later (BNPL) arrangement.

While credit cards still have a solid foothold, layaway plans are becoming a thing of the past.BNPL programs managed by third-party credit specialistsare becoming more popular and accessible. In fact, as many as 25% of Americans have used BNPL as an option,according to one survey.

And though retailers don’t get to charge interest to customers using BNPL (in fact, they’re charged a fee by the BNPL vendors), they’re making up for it inincreased sales volume.

Table of Contents

What is buy now, pay later (BNPL)?

A buy now, pay later plan is a loan offered to a customer at the point of sale so they can purchase merchandise on credit but without a credit card. Popular options includeShop Pay Installmentsfrom Shopify, Affirm, Afterpay, Sezzle, PayPal, and Klarna.

许多人会运行一个即时软信贷检查customer (the type that doesn’t affect your credit score), and then release funds for a point-of-sale loan. Customers have different options for paying off the loan balance, which typically depend on the company used and the amount borrowed; some payment options incur interest, but others do not, and some companies charge late fees or fees for missed payments. BNPL companies may offset the lack of interest charged to the consumer with a fee that they charge the retailer.

Boost sales with buy now, pay later

Shop Pay Installments gives customers flexibility at checkout by letting them pay in four interest-free payments or monthly installments for up to 12 months. Increaseaverage order values, reduce abandoned carts, and turn more browsers into buyers today.

Discover Shop Pay InstallmentsHow BNPL works, in 5 steps

Here’s how the BNPL process works for both consumers and retailers, in five steps.

- A customer shops as normal and begins the checkout process.If you’re a customer, you start the BNPL process as you would any other ecommerce transaction. You shop your favorite online stores, select merchandise, and prepare to pay.

- The retailer’s chosen BNPL vendor presents the option to buy now and pay later.During checkout, the customer will have the option to purchase using BNPL, along with other purchase options like credit or debit cards.

- The lender runs asoft credit checkon the customer.When the customer opts to purchase their items using BNPL, they enter some personal details with the BNPL lender (such as a full address or Social Security number). The lender immediately runs a soft credit check on the customer to get assurance that they will eventually pay back their loan, based on their credit history. This type of credit check does not get reported to the credit bureaus, so it will not dent credit scores like a full credit check might.

- The BNPL vendor charges a fee to the retailer.The BNPL vendor will take a percentage of the retail transaction, which is billed directly to the retailer. The fee (which typically ranges between 2% and 8%) gets deducted from the sum the BNPL lender remits to the merchant. This is similar to the arrangements that traditional credit card companies have with retailers.

- The customer pays off the balance over time.如果大多数BNPL厂商提供无息支付a customer pays their full balance in a short period of time (typically 30 days). If customers need more time to pay down their balance, the lenders offer different payment plans with different interest rates. Much like with a credit card, the faster the customer pays off the bill, the less total interest they pay.

4 advantages of BNPL for customers

Consumers enjoy several potential benefits when using a BNPL service.

No credit card needed

BNPL is an equalizer for those without credit cards. A BNPL service offers many of the same benefits as a credit card, but for smaller, individual purchases. Customers can even use a BNPL service like a credit card by requesting a virtual card number in advance of their purchase. This card number will cover the exact amount of money needed to complete the purchase. They can do all of this on the BNPL vendor’s website or via its smartphone app.

Flexibility

BNPL offers flexible payment options. Most BNPL services offer options to customers at the point of sale. Customers can pay the full purchase price using the BNPL service or split the purchase between BNPL and some other payment source (like a debit card).

Interest-free

As many as15% of Americanshave actually stopped using credit cards altogether, largely due to high interest rates. It’s no surprise, considering average interest rates havesurpassed 20%. BNPL offers options for interest-free payments. If a customer chooses a short loan period and makes payments on time, they can borrow money without paying any interest.

No credit history impact

Soft credit checks have no impact on your credit. Most BNPL vendors run soft credit checks on their clients to affirm their eligibility for a loan. Unlike a hard credit check, this will not dent your credit score. On the other hand, if you are late in your payments to your BNPL vendor, this does get reported to credit bureaus, much like when you’re late on credit card payments.

6 popular BNPL services

Retailers regard buy now, pay later services favorably because they’ve been shown to boost overall sales volume. As a result of this retailer preference, there are more viable BNPL services than ever before. Here are six well-regarded options.

1. Shop Pay Installments

Shopify offers a robust BNPL service, calledShop Pay Installments, in partnership with Affirm, using the same network of lending partners. Shop Pay Installments grants online small businesses the same BNPL benefits enjoyed by major retailers, including a largeraverage order valueand less cart abandonment.

If you choose Shopify as your ecommerce platform, you can use Shop Pay Installments to let customers pay in one of two ways, depending on the transaction amount:

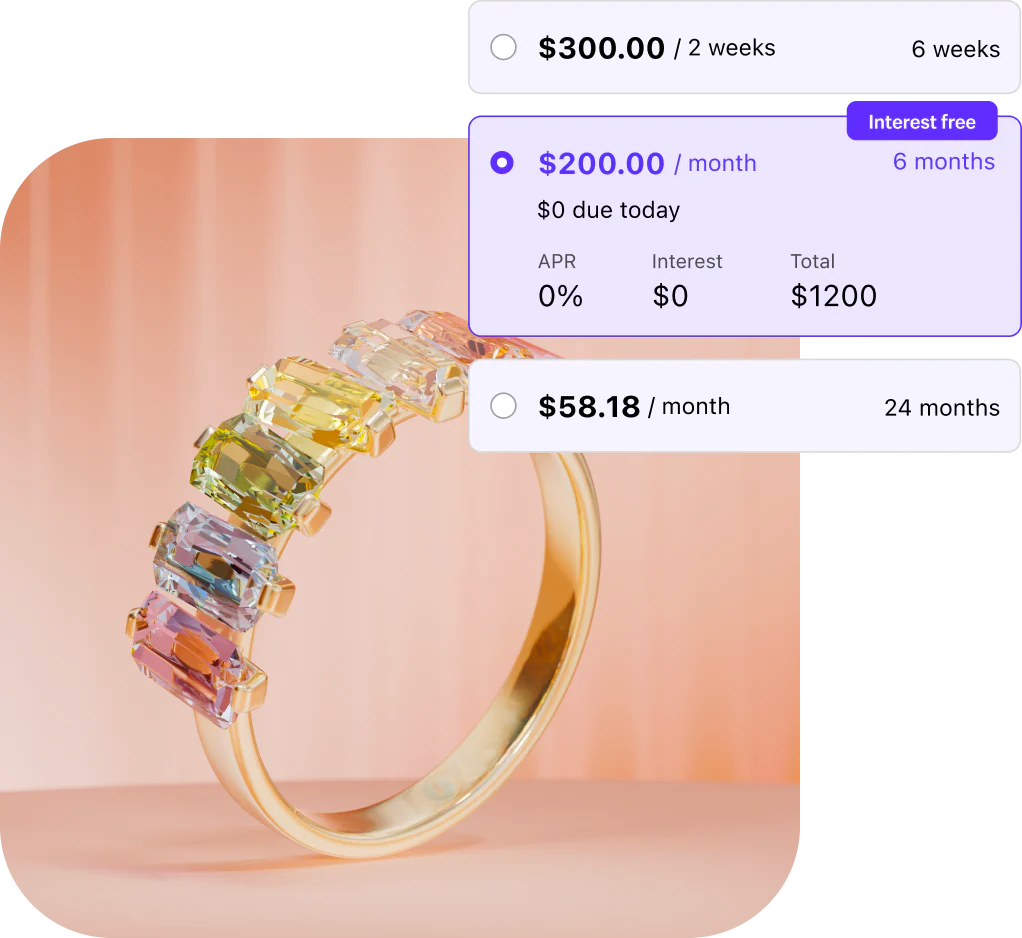

- For orders from $50 to $999.99: Customers pay four biweekly, interest-free payments.

- For orders from $150 to $17,500:客户支付每月,国米est-bearing, from 10% to 36% APR. These may be paid in three, six, or 12 months, depending on the purchase amount.

To check your eligibility, log in to your Shopify admin and go toSettings>Payments. ClickManageunderShop Pay Installments. If you’re eligible for the premium package, clickSelect premium packageto accept the premium financing options on offer.

To activate Shop Pay Installments on your Shopify store, do the following:

- From your Shopify admin, go toSettings>Payments.

- In the Shopify Payments section, clickManage.

- In theShopPaysection, checkShopPayInstallments, and then clickSave.

You can alsouse Shop Pay Installments with Shopify POSfor in-person transactions.

2. Affirm

Affirm is offered as a payment option at big retailers like Amazon and Target for amounts up to $17,500. For short-term loans (four payments with two weeks between each payment), Affirm charges no interest and no fees. Longer-term loans require interest payments (ranging from 10% to 30% APR, depending upon your credit) but no fees.

3. Afterpay

Afterpay has a smart credit limit tool that creates a spending limit for shoppers based on their personal credit history. This ideally prevents them from spending more than they can pay back. It also offers consistent reminders to make payments, and its virtual card service is easy to use. Afterpay charges late fees, and its interest rates fall into the same 10% to 30% range as Affirm.

4. Sezzle

Sezzle has a feature that lets customers push back payment due dates by up to two weeks. Sezzle requires a 25% down payment on all purchases, but you can pay off most loans without owing interest. It has more than 44,000 retail partners, but it’s less popular among larger retailers.

5. PayPal

PayPal is probably better known as a secure online payment system or as a person-to-person cash transfer app, but it’s also a BNPL lender. Its signature lending product is an interest-free service called Pay in 4, which breaks transactions into four scheduled payments. PayPal limits this service to purchases between $30 and $1,500. PayPal’s standard interest rate is roughly 24% APR.

6. Klarna

Klarna uses a proprietary metric it calls Purchase Power instead of strict borrowing limits. It describes Purchase Power as “an estimated amount based on factors such as your payment history with Klarna and your outstanding balance.” If you have good credit and a solid payment history, you may be eligible for larger point-of-sale loans from Klarna than from most other BNPL vendors. When you pay interest, it will max out at 25%.

Alternatives to BNPL

BNPL may not be an option for every small business merchant. Here are some alternatives for both businesses and shoppers to explore:

- Layaway:如果您的业务可以处理它,你仍然可以的fer the layaway option. With this setup, customers have to pay the full amount in installments before they can receive the product.

- Personalloan: If a shopper really can’t afford something, and BNPL or credit cards aren’t options, they can opt for a personal loan. It’s not your role as a merchant to suggest this—leave the decision up to the customer.

- 客户loyaltyprogramincentives你可能有一个顾客忠诚度课题am that offers rewards for purchases. You can consider offering discounts or allowing customers to “pay” for a purchase with loyalty program points.

- Income-basedpricing: Some businesses have an income-based pricing system that allows customers to pay what they can. This can be a sensitive and tricky topic to navigate, and it also requires a lot of trust in your customers.

- Store credit card: Many major retailers offer their own branded credit cards. While this may not be an accessible route for small businesses, it can potentially be an option once your business grows.

Moving forward with BNPL in your business

Offering more payment options gives your customers more chances to make a purchase. And that means more conversions and higher sales.

With Shopify Pay Installments, you can offer BNPL to all your customers—and make it easier for them to pay for their purchase. You can give shoppers more flexibility at checkout, both online and in-store. There are no hidden fees, and you get paid upfront, regardless of the payment schedule they choose.Learn more about Shop Pay Installments.